On... The Power of Super

Wealth is like a bucket of leaking water - you need to constantly fill it up or it will run dry.

I spoke to a friend and he thinks as long as you work hard and earn lots of money, you can outsource your financial management to your Superfund. Whilst some other people think that you should manage your own wealth. I don't have a strong opinion but I tend to favour the latter. Since it's your bucket, who better to look after it? I ran some numbers for comparison with the following assumptions.

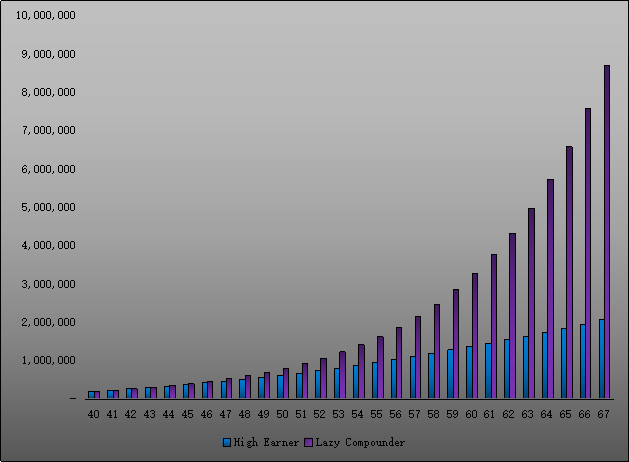

High Earner has a Lifetime Average Salary of 200K per year with 10% Super contribution. His Superfund returns 6% after fees annually. Lazy Compounder earns enough money just for living expenses - although he spends most of his time managing his investment resulting in returns of 15% annually. Assume they both have 200K invested by the age of 40. Let's see how they fare over the next 20+ years.

The chart above shows their net worth by age. By the time they retire (roughly 60),Lazy Compounders net worth is almost 3 times High Earner's. Not a bad result for Lazy Compounder. The next chart shows their returns/earnings by age.

Again, we clearly have a winner. Although there's a caveat - High Earner has a salary of 200K annually, which he can spend comfortably. Lazy Compounder cannot spend any of his returns if he wants to grow his account. Let's zoom in and see how they fare after retirement.

I guess my friend is right, you can have a comfortable retirement living off your Superfund just like High Earner - with 80K annually from his Superfund (roughly 40K is enough for me, so 80K is quite good). However, Lazy Compounder is doing it much better, so it might be worth looking after your own bucket. Anyway, your bucket, your call.

I spoke to a friend and he thinks as long as you work hard and earn lots of money, you can outsource your financial management to your Superfund. Whilst some other people think that you should manage your own wealth. I don't have a strong opinion but I tend to favour the latter. Since it's your bucket, who better to look after it? I ran some numbers for comparison with the following assumptions.

High Earner has a Lifetime Average Salary of 200K per year with 10% Super contribution. His Superfund returns 6% after fees annually. Lazy Compounder earns enough money just for living expenses - although he spends most of his time managing his investment resulting in returns of 15% annually. Assume they both have 200K invested by the age of 40. Let's see how they fare over the next 20+ years.

The chart above shows their net worth by age. By the time they retire (roughly 60),Lazy Compounders net worth is almost 3 times High Earner's. Not a bad result for Lazy Compounder. The next chart shows their returns/earnings by age.

Again, we clearly have a winner. Although there's a caveat - High Earner has a salary of 200K annually, which he can spend comfortably. Lazy Compounder cannot spend any of his returns if he wants to grow his account. Let's zoom in and see how they fare after retirement.

I guess my friend is right, you can have a comfortable retirement living off your Superfund just like High Earner - with 80K annually from his Superfund (roughly 40K is enough for me, so 80K is quite good). However, Lazy Compounder is doing it much better, so it might be worth looking after your own bucket. Anyway, your bucket, your call.

Comments

Post a Comment