On... Learning to Fish

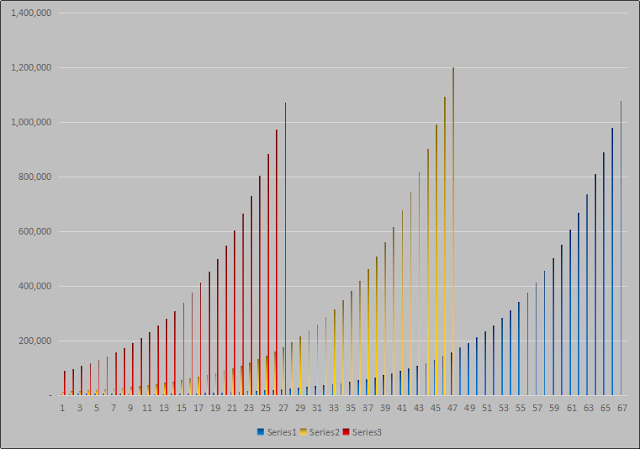

Contrary to the title, this post is not about fishing. Having gone fishing only once, there's not much I can share about fishing. What the post is about is the saying that goes "Give me a fish and it lasts me a day, teach me to fish and it will lasts me a lifetime, ". You see, my friend who had recently went on to the app Spaceship voyager had been sharing his equity returns with me and the results were astounding. A quick check on the Spaceship voyager website shows that the fund has been compounding north of 20% P. A. Note that I am not recommending to invest with Spaceship voyager - I don't have an opinion for or against ( Do Your Own Research ). The question is - Why should I do my own investing?, rather than just allocate my capital to a fund manager who can compound my returns at a high rate. As a fellow investor would point out to me "Do you want to be right or do you want to make money? ". At the end of the day, of course I want to make money. But ...